How to Automate Enterprise Risk and Compliance Monitoring Using Multi-Agent AI Systems

$150.00

| System Name: |

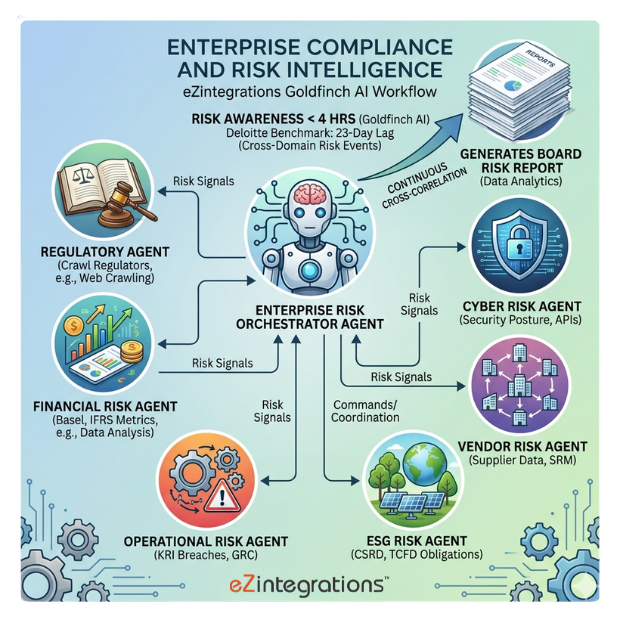

Enterprise Compliance and Risk Intelligence |

|---|---|

| Architecture: |

Hierarchical Multi-Agent System – 1 Enterprise Risk Orchestrator (Coordinator) + 6 specialized Worker Agents (Regulatory; Financial Risk; Operational Risk; Cyber Risk; Vendor Risk; ESG Risk) operating through continuous cross-domain risk signal aggregation; event-based inter-agent correlation; shared enterprise risk vector knowledge base; and human-in-the-loop escalation gates for material risk events; 7 total agents |

| Coordinator Agent: |

Enterprise Risk Orchestrator – continuously receives risk signal events from all 6 Worker Agents; cross-correlates risk signals across domains (e.g. a regulatory change that increases financial risk exposure that coincides with a vendor risk event is scored as a compound risk); computes the enterprise risk score across all domains; determines which compound risk events require Board or CRO escalation; and assembles the automated Board Risk Report from the aggregated multi-agent risk intelligence |

| Safety Layer: |

Human-in-the-loop gate triggers when: Enterprise Risk Orchestrator computes a compound risk event above the configured Critical severity threshold (e.g. regulatory + financial + vendor risk simultaneously breaching thresholds) – CRO review required before Board escalation; Regulatory Agent identifies a new regulatory requirement with a compliance deadline within 90 days – CCO sign-off required on the compliance response plan; Financial Risk Agent detects a breach of a hard regulatory risk limit (Basel III LCR below minimum; VaR above board-approved limit) – CFO and CRO immediate notification required; Orchestrator cross-domain confidence falls below 0.75 on any compound risk assessment. Max 3 retries before CRO escalation with full agent context. All HITL decisions logged with reviewer identity; decision rationale; and timestamp for regulatory audit documentation (Basel; DORA; FDA). |

| Extensibility Note: |

Beyond the 9 native Goldfinch AI tools; users can add custom tools self-service – including sanctions screening APIs (OFAC; UN; EU); geopolitical risk intelligence feeds (Moody’s Analytics; Verisk Maplecroft); actuarial risk modeling connectors; insurance coverage verification APIs; and internal audit management system connectors. |

| On-Premise Supported: |

Yes – eZintegrations connects to on-premises systems (SAP GRC on-prem; ServiceNow GRC on-prem; Oracle GRC on-prem; financial risk management systems on-prem; internal SIEM on-prem; and others) via IPSec Tunnel. eZintegrations is a browser-based; cloud-hosted platform and does not require any on-premises software installation. |

| Tags: |

Goldfinch AI risk compliance; enterprise risk management AI; multi-agent GRC system; regulatory monitoring AI agent; financial risk AI agent; cyber risk intelligence AI; vendor risk AI agent; ESG risk monitoring AI; board risk report automation; DORA compliance AI; Basel III risk AI; GRC automation Goldfinch AI |

| AI Credits Required: |

Yes – Goldfinch AI agentic systems consume credits across the Enterprise Risk Orchestrator and all 6 Worker Agents per risk monitoring cycle, per document analysis, per regulatory publication processed, and per reflection/retry loop. |

| Worker Agents: |

Operational Risk Agent: Monitors Key Risk Indicators (KRIs) from the GRC platform (ServiceNow GRC or SAP GRC) and operational data sources – detecting KRI breaches, process failure signals, and incident trends across business lines, and classifying operational risk events by severity and regulatory reporting requirement; Cyber Risk Agent: Monitors the organization’s security posture and external threat intelligence feeds – querying the cyber risk platform (e.g. BitSight, SecurityScorecard) for vendor and internal security scores, tracking vulnerability exposure, and correlating cyber risk events with regulatory requirements (DORA, NIST CSF, ISO 27001) from the Knowledge Base, Regulatory Agent: Monitors regulatory publications, amendments, and enforcement actions from configured regulatory bodies (Basel Committee, EBA, DORA, FDA, ICH, OSHA, SEC, FCA, and others) via Web Crawling – classifying each change by applicability to the organization, compliance deadline, required action, and estimated compliance cost; Financial Risk Agent: Monitors credit risk, market risk, and liquidity risk signals from the financial DW and market data feeds – computing risk metrics (VaR, CVaR, credit concentration, liquidity coverage ratio) against configured regulatory thresholds (Basel III/IV, DORA, IFRS 9) and flagging breaches or approaching-threshold conditions, Vendor Risk Agent: Monitors third-party and supplier risk signals from the SRM platform and external vendor risk databases – tracking supplier financial health, concentration risk, regulatory compliance status, and cyber risk score changes for the organization’s critical vendor population; ESG Risk Agent: Monitors climate-related risk signals, supply chain ESG exposure, and regulatory ESG reporting requirements (CSRD, TCFD, SEC climate disclosure) – computing ESG risk scores per vendor and geography and flagging material ESG events that affect the organization’s regulatory disclosure obligations or ESG-linked financing covenants |

| Goldfinch AI Native Tools Used: |

API Tool Call: All 6 Worker Agents use API Tool Call – Financial Risk Agent (DW risk metrics query, market data API), Operational Risk Agent (ServiceNow GRC https://docs.servicenow.com/en-US/bundle/washingtondc-governance-risk-compliance/ or SAP GRC https://help.sap.com/docs/SAP_GOVERNANCE_RISK_COMPLIANCE KRI breach query), Cyber Risk Agent (BitSight or SecurityScorecard API for vendor and internal security scores), Vendor Risk Agent (SRM platform supplier financial health data, Dun and Bradstreet risk scores), ESG Risk Agent (ESG data provider APIs – MSCI ESG, Refinitiv ESG, Supply Chain ESG exposure data); Orchestrator (enterprise risk score write to GRC and DW, Board Report delivery), Data Analysis: Financial Risk Agent computes VaR, CVaR, credit concentration, and liquidity coverage ratio from DW data; Operational Risk Agent scores KRI breach severity and business line exposure; Cyber Risk Agent computes security posture score and regulatory compliance gap; Vendor Risk Agent computes vendor concentration risk and third-party exposure score; ESG Risk Agent computes ESG risk score per vendor and regulatory disclosure gap; Orchestrator computes cross-domain enterprise risk score and compound risk severity; Document Intelligence: Regulatory Agent analyzes full regulatory publication text – extracting applicability scope, compliance deadline, required action, penalty provisions, and cross-reference to existing compliance framework gaps; Vendor Risk Agent analyzes vendor financial statements, audit reports, and regulatory filings for risk signal extraction, Integration Workflow as Tool: Orchestrator calls pre-built sub-workflows – GRC incident record creation for material risk events (ServiceNow GRC or SAP GRC), Board Risk Committee meeting notification sub-workflow, regulatory compliance task assignment sub-workflow (routes compliance response actions to the relevant business line owner), and Snowflake DW risk score write sub-workflow, Knowledge Base Vector Search: All 7 agents share a persistent enterprise risk knowledge base containing: applicable regulatory requirements per jurisdiction and business line, historical risk event precedents and outcomes, risk appetite statements and board-approved thresholds per risk domain, compliance obligation matrices, vendor criticality classifications, ESG reporting frameworks (CSRD, TCFD, SFDR), and prior Board Risk Report narratives – each agent retrieves context relevant to its current risk domain assessment; Data Analytics with Charts/Graphs/Dashboards: Enterprise Risk Orchestrator generates the Board Risk Report dashboard – enterprise risk score trend, risk heat map by domain and business line, regulatory compliance deadline calendar, top 10 risk events by severity, vendor risk concentration map, ESG risk exposure by geography, and financial risk metric trend charts; also generates the CRO weekly risk intelligence brief, Watcher Tools: Enterprise Risk Orchestrator continuously monitors all 6 Worker Agent risk signal feeds – triggering cross-domain correlation within 60 minutes of any material risk event publication; also monitors GRC platform event queues and regulatory database update feeds for new publications; Web Crawling: Regulatory Agent crawls regulatory body websites (Basel Committee https://www.bis.org/bcbs/, EBA https://www.eba.europa.eu/, DORA publications, FDA https://www.fda.gov/, ICH https://www.ich.org/, SEC https://www.sec.gov/, FCA https://www.fca.org.uk/, OSHA https://www.osha.gov/) for new publications, amendments, guidance, and enforcement actions; ESG Risk Agent crawls CSRD regulatory publications, TCFD framework updates, and SEC climate disclosure guidance |

Table of Contents

| Planning: |

The Enterprise Risk Orchestrator uses continuous event-driven goal decomposition – when any Worker Agent publishes a material risk event; the Orchestrator immediately evaluates whether the event creates compound risk exposure across other domains (e.g. a DORA regulatory change combined with a Cyber Risk Agent security posture gap creates a compound regulatory-plus-cyber risk event requiring immediate escalation). Schema-driven rules govern risk scoring thresholds and escalation criteria per domain; LLM reasoning governs cross-domain compound risk assessment; regulatory applicability analysis; and Board Risk Report narrative generation. |

|---|---|

| Messaging: |

All 7 agents communicate via structured risk event messages – each Worker Agent publishes a structured risk event (domain; severity; affected business lines; regulatory implication; time sensitivity) that the Orchestrator ingests; cross-correlates with all other active risk signals; and evaluates against the enterprise risk appetite from the Knowledge Base. Material compound risk events trigger immediate CRO notification; routine risk updates accumulate in the weekly Board Risk Report. |

| Reflection: |

The Orchestrator applies a reflection loop before publishing any compound risk assessment or Board escalation – if cross-domain confidence falls below 0.75; the Orchestrator re-queries the Knowledge Base for relevant risk appetite statements and historical precedents; re-evaluates the cross-domain correlation; and retries up to 3 times before escalating to the CRO with an uncertain flag. The Regulatory Agent applies additional reflection when a regulatory publication has ambiguous applicability scope – retrieving additional regulatory context before classifying the organization’s compliance obligation. |

| Knowledge: |

All 7 agents share a persistent enterprise risk vector knowledge base containing: applicable regulatory requirements per jurisdiction and business line (Basel III/IV; DORA; FDA 21 CFR; ICH Q10; IFRS 9; CSRD; TCFD; SFDR; NIST CSF; ISO 27001); risk appetite statements and board-approved thresholds per risk domain; historical risk event precedents and resolution outcomes; compliance obligation matrices per regulation; vendor criticality classifications; ESG reporting frameworks; and prior Board Risk Report narratives for comparison and trend context. Indexed by risk domain; jurisdiction; business line; and regulatory framework. |

| Execution: |

Each Worker Agent executes continuous monitoring within its configured risk domain using its designated Goldfinch AI tools – Web Crawling for regulatory and ESG publications; API Tool Call for GRC; financial DW; cyber risk; and vendor risk data sources; Data Analysis for risk metric computation; and Document Intelligence for regulatory and vendor document analysis. The Orchestrator aggregates all domain risk scores into a single enterprise risk score; writes it to the GRC platform and Snowflake DW via Integration Workflow as Tool; and generates the Board Risk Report dashboard via Data Analytics on the configured Board Risk Committee reporting schedule. |

| Business Impact: |

Deloitte Global Risk Management Survey: organizations with integrated multi-domain risk monitoring reduce the time from risk emergence to executive awareness from an average of 23 days to under 4 hours. DORA (Digital Operational Resilience Act) requires continuous ICT risk monitoring with sub-24-hour incident reporting for EU financial institutions from January 2025. The Basel Committee’s Principles for Effective Risk Data Aggregation require near-real-time risk data aggregation for systemically important banks. The Goldfinch AI risk compliance hub meets these regulatory mandates while simultaneously monitoring 6 risk domains that no single GRC platform monitors autonomously. |

The Goldfinch AI risk compliance hub from eZintegrations deploys 7 coordinated AI agents — an Enterprise Risk Orchestrator plus 6 specialized Worker Agents — to continuously monitor regulatory changes, financial risk metrics, operational KRI breaches, cyber security posture, vendor risk signals, and ESG exposure across all domains simultaneously, computing a live enterprise risk score and generating the Board Risk Report automatically. eZintegrations is an enterprise automation platform covering iPaaS, AI Workflows, AI Agents, and Goldfinch AI agentic automation.

What Is Goldfinch AI Risk Compliance Automation?

Goldfinch AI risk compliance automation is a hierarchical multi-agent system where an Enterprise Risk Orchestrator receives risk signals from 6 domain-specific Worker Agents simultaneously and cross-correlates them to compute a compound enterprise risk score. Unlike GRC platforms that record risk events for Risk Managers to assess manually, the Goldfinch AI risk compliance hub autonomously monitors all 6 risk domains 24/7, detects cross-domain compound risk events that no single-domain tool can identify, and generates Board-ready risk intelligence within hours of any material risk event — not the 23-day average lag documented by Deloitte for manual risk management processes.

How Does Goldfinch AI Risk Compliance Automation Use 7 Agents to Monitor Regulatory, Financial, Cyber, Vendor, Operational, and ESG Risk and Generate a Continuous Enterprise Risk Score?

The Regulatory Agent crawls regulatory bodies via Goldfinch AI Web Crawling. The Financial Risk Agent computes Basel and IFRS 9 metrics from the DW. The Operational Risk Agent monitors GRC KRI breaches. The Cyber Risk Agent queries security posture APIs. The Vendor Risk Agent monitors SRM and D&B supplier risk data. The ESG Risk Agent monitors CSRD and TCFD reporting obligations. The Enterprise Risk Orchestrator cross-correlates all 6 domain signals and computes the enterprise risk score via Goldfinch AI Data Analysis. The Board Risk Report is generated via Data Analytics.

Goldfinch AI ships with 9 native out-of-the-box agent tools. Users can add custom tools self-service beyond the 9 native tools. This Goldfinch AI risk compliance hub compresses the risk-emergence-to-executive-awareness window from 23 days (Deloitte benchmark) to under 4 hours across all 6 risk domains simultaneously.

Watch Demo

| Video Title: |

Goldfinch AI Risk Compliance Hub | 7 Agents; Continuous Enterprise Risk Score from Regulatory; Financial; Cyber; Vendor; and ESG Monitoring |

|---|---|

| Duration: |

7 to 10 minutes |

Outcome & Benefits

| Autonomy: |

90%+ of risk monitoring and risk event classification handled autonomously across all 6 domains; material compound risk events and regulatory deadline breaches route to CRO/CCO for human review; Board Risk Report generated automatically on the configured reporting schedule without Risk Manager manual compilation |

|---|---|

| Time Saved: |

Risk-emergence-to-executive-awareness from 23 days (Deloitte manual benchmark) to under 4 hours; Board Risk Report preparation from 3 to 5 days of manual compilation across 6 functions to automated generation; regulatory publication review from weekly manual scan (catching 40 to 60% of relevant publications) to continuous automated monitoring (100% coverage) |

| Cost Reduction: |

30 to 40% reduction in GRC operational cost from automated risk monitoring (Gartner GRC automation benchmark); regulatory penalty avoidance from 100% regulatory deadline coverage; estimated $500K to $5M per avoided regulatory enforcement action (median EU financial regulatory fine 2023: 1.4M euro per ESMA); DORA non-compliance penalty: up to 1% of total annual global turnover for EU financial institutions |

| Reliability: |

100% of configured regulatory body publications monitored continuously; zero missed KRI breaches through continuous Operational Risk Agent GRC monitoring; financial risk metrics updated every 4 hours against hard regulatory limits; enterprise risk score updated within 60 minutes of any material domain event |

Performance Metrics

| KPI | Before | After | Impact |

|---|---|---|---|

| Risk-to-Executive Awareness | 23 days average (Deloitte) | Under 4 hours | 99%+ faster |

| Regulatory Publication Coverage | 40 to 60% (manual scan) | 100% continuous | Full coverage |

| Board Risk Report Preparation | 3 to 5 days manual | Automated on schedule | Full automation |

| Cross-Domain Risk Correlation | None (siloed domain tools) | Continuous compound scoring | New capability |

| DORA ICT Incident Reporting | Manual (24-hour risk) | Sub-4-hour automated detection | Regulatory compliance |

| GRC Operational Cost | Baseline | 30 to 40% reduction (Gartner) | Significant FTE reallocation |

Technical Details

| Planner Type: |

Continuous event-driven planning with LLM-hybrid cross-domain correlation – the Enterprise Risk Orchestrator uses schema-driven rules for single-domain risk threshold breaches (deterministic: VaR above board limit triggers CFO notification; LCR below minimum triggers immediate escalation) and LLM reasoning for cross-domain compound risk assessment, regulatory applicability analysis, Board Risk Report narrative generation, and compound risk scoring where multiple domain signals create an emergent risk that exceeds the individual domain severity. |

|---|---|

| Scheduling: |

Enterprise Risk Orchestrator runs continuously via Watcher Tools (60-minute cross-domain correlation cycle; immediate trigger on any Critical-severity risk event); Regulatory Agent crawls all configured regulatory body sites daily (immediate crawl on high-priority regulatory body announcement detection); Financial Risk Agent runs every 4 hours and immediately on hard regulatory limit approach (within 10% of board-approved VaR or LCR limit); Operational Risk Agent monitors GRC KRI feeds in near-real-time (15-minute polling); Cyber Risk Agent queries security APIs daily and immediately on material security score change; Vendor Risk Agent runs weekly financial health check and immediately on material supplier risk event; ESG Risk Agent runs weekly CSRD/TCFD publication scan and quarterly ESG score computation; Board Risk Report generates on the configured Board Risk Committee schedule (default: monthly; quarterly; and on-demand). |

| Tool Router: |

The Enterprise Risk Orchestrator aggregates all 6 Worker Agent risk event outputs continuously. For single-domain events below the compound risk threshold; the Orchestrator routes to the relevant domain owner for awareness (Regulatory Agent finding to CCO; Financial Risk Agent breach to CFO; Cyber Risk event to CISO). For cross-domain compound risk events above the compound threshold; the Orchestrator routes to CRO with the full multi-domain briefing. Each Worker Agent selects its tools based on its domain monitoring task: Web Crawling for regulatory and ESG publications; API Tool Call for structured risk data from GRC; financial DW; cyber risk; vendor risk platforms; Data Analysis for risk metric computation; Document Intelligence for regulatory and vendor document analysis; Knowledge Base for risk appetite and threshold context. |

| Evaluation Metrics: |

Enterprise risk score trend (per domain and composite; updated every 4 hours); regulatory publication monitoring coverage rate (% of configured bodies monitored with zero publication gaps); regulatory deadline compliance rate (% of compliance obligations met on time); financial risk metric accuracy vs. regulatory computation (internal validation vs. regulator-submitted figures); KRI breach detection time (minutes from GRC event creation to Orchestrator awareness); Board Risk Report completeness and on-time delivery rate; compound risk event false positive rate (CRO-reviewed events confirmed as material vs. agent-flagged). |

| Auditability: |

Every agent action is logged with: agent name; risk domain; monitoring source; risk event detected; document reference or API source; Data Analysis confidence score; cross-domain correlation result; escalation routing decision; HITL status (autonomous assessment or CRO/CCO/CFO-reviewed); and timestamp. The Enterprise Risk Orchestrator maintains a continuous enterprise risk event log per domain and per compound event. Compliance and audit teams access the full risk event log and Board Risk Report history via the Goldfinch AI audit dashboard – exportable to Snowflake DW for regulatory submission and long-term retention. For regulated entities: the regulatory monitoring log documents which regulatory publications were reviewed; when; and what compliance obligation was identified – directly supporting regulatory examination readiness. DORA ICT incident audit trail: all cyber risk events; detection times; and response actions are logged per DORA Article 17 and 19 requirements. |

| Agent Roles: |

Cyber Risk Agent: API Tool Call (BitSight https://www.bitsight.com/ or SecurityScorecard https://securityscorecard.com/ vendor and internal security scores, SIEM integration), Data Analysis (security posture score, regulatory compliance gap vs. DORA/NIST CSF/ISO 27001), Knowledge Base Vector Search (cyber risk appetite, DORA ICT risk requirements); Vendor Risk Agent: API Tool Call (SRM platform supplier data, Dun and Bradstreet https://www.dnb.com/ supplier financial health API, cyber risk platform vendor scores), Data Analysis (vendor concentration risk, third-party exposure score, financial distress signals), Knowledge Base Vector Search (vendor criticality classifications, third-party risk appetite), Enterprise Risk Orchestrator (Coordinator): continuous cross-domain risk signal correlation, compound risk scoring, CRO/CCO/CFO escalation routing, Board Risk Report generation, GRC platform risk score write; Regulatory Agent: Web Crawling (Basel Committee https://www.bis.org/bcbs/, EBA, DORA, FDA, ICH, SEC, FCA, OSHA, ESMA, and configured bodies), Document Intelligence (regulatory publication full-text analysis), Data Analysis (applicability and compliance gap scoring), Knowledge Base Vector Search (compliance obligation matrix, regulatory deadline calendar), ESG Risk Agent: Web Crawling (CSRD regulatory publications https://finance.ec.europa.eu/capital-markets-union-and-financial-markets/company-reporting-and-auditing/company-reporting/corporate-sustainability-reporting_en, TCFD framework updates, SEC climate disclosure guidance), API Tool Call (MSCI ESG data API, Refinitiv ESG, supply chain ESG exposure data), Data Analysis (ESG risk score per vendor and geography, regulatory disclosure gap), Knowledge Base Vector Search (CSRD/TCFD/SFDR requirements, ESG-linked financing covenant terms), Financial Risk Agent: API Tool Call (Snowflake DW https://docs.snowflake.com/ financial risk metrics, Bloomberg/Refinitiv market data API), Data Analysis (VaR, CVaR, credit concentration, LCR, NSFR per Basel III/IV https://www.bis.org/bcbs/basel3.htm), Knowledge Base Vector Search (board-approved risk thresholds, IFRS 9 https://www.ifrs.org/issued-standards/list-of-standards/ifrs-9-financial-instruments/ methodology); Operational Risk Agent: API Tool Call (ServiceNow GRC https://docs.servicenow.com/en-US/bundle/washingtondc-governance-risk-compliance/ or SAP GRC https://help.sap.com/docs/SAP_GOVERNANCE_RISK_COMPLIANCE KRI data), Data Analysis (KRI breach severity and business line exposure scoring), Knowledge Base Vector Search (KRI thresholds, operational risk appetite) |

Connectivity and Deployment

| Supported Protocols: |

REST API (ServiceNow GRC; SAP GRC; Bloomberg/Refinitiv market data API; BitSight/SecurityScorecard cyber risk API; Dun and Bradstreet vendor risk API; MSCI ESG/Refinitiv ESG data API; Snowflake DW); Web Crawling (Basel Committee; EBA; DORA; FDA; ICH; SEC; FCA; ESMA; OSHA; CSRD; TCFD regulatory body sites and publication feeds); SMTP (CRO/CCO/CFO risk event notifications; Board Risk Report distribution; compliance task assignment notifications); HTTPS; OAuth 2.0; IPSec Tunnel (on-premises GRC platform; SIEM; and financial risk management system connectivity) |

|---|---|

| Security & Compliance: |

SOC Type II certified; GDPR-compliant risk data handling (customer data in credit risk computations handled under GDPR Article 6 legitimate interest for financial risk management; data minimization applied per agent); DORA Article 17 and 19-compliant ICT risk monitoring audit trail for EU financial institutions; HIPAA-eligible configuration for healthcare risk management (patient-data-adjacent operational risk monitoring); Basel BCBS 239-compliant risk data aggregation (near-real-time risk data aggregation with full provenance documentation for systemically important banks). RBAC enforced: CRO has full enterprise risk view; domain Risk Managers access only their domain’s risk data; Board Risk Committee receives the Board Risk Report only (not underlying risk data); Audit team has read-only access to the full event log and audit trail. |

| Tenancy Model: |

Both single-tenant and multi-tenant deployments are supported. Single-tenant is mandatory for systemically important banks; regulated financial institutions; and pharmaceutical companies where enterprise risk data; regulatory examination materials; and Board Risk Committee reports are subject to strict confidentiality; attorney-client privilege; and regulatory data residency requirements. Single-tenant provides dedicated infrastructure with full data segregation and configurable data residency per jurisdiction (EU; US; UK; APAC). |

| On-Premise Supported: |

Yes – eZintegrations connects to on-premises systems (SAP GRC on-prem; ServiceNow GRC on-prem; Oracle GRC on-prem; financial risk management systems on-prem; internal SIEM on-prem; and others) via IPSec Tunnel. eZintegrations is a browser-based; cloud-hosted platform and does not require any on-premises software installation. |

AI Credits

| Credit Consumption Model: |

Continuous daily monitoring cycle (Regulatory; Financial Risk; Operational Risk; Cyber Risk Agents); weekly cycle (Vendor Risk; ESG Risk Agents); Board Risk Report generation on configured schedule; event-triggered immediate response for Critical-severity risk events; reflection/retry overhead at approximately 10 to 15% Estimated Credits per End-to-End Run: Daily risk intelligence cycle (all 7 agents; no material risk events): ~80 to 150 credits per day Daily cycle with 1 material compound risk event (CRO escalation; Board Report update): ~150 to 250 credits per day Monthly Board Risk Report generation cycle: ~200 to 400 credits per report (full multi-domain narrative + dashboard generation) Weekly cycle cost (5 daily cycles + Vendor Risk weekly + ESG weekly): ~600 to 1,200 credits per week |

|---|---|

| Retry / Reflection Credit Cost: |

Each Orchestrator reflection/retry cycle: ~6 to 10 additional credits per retry. Regulatory Agent reflection on ambiguous applicability: ~5 to 8 credits per reflection. At 10% complex event rate; add approximately 12 to 18% to the monthly estimate. |

| Monthly Credit Estimate (at Typical Volume): |

Regional bank or mid-market financial services (5 to 10 regulatory bodies monitored; standard risk domains): ~5,000 to 10,000 credits per month Large financial institution (15 to 25 regulatory bodies; global multi-jurisdiction): ~12,000 to 25,000 credits per month Global systemically important bank or large pharma (30+ regulatory bodies; all 6 domains; multi-entity): ~25,000 to 50,000 credits per month |

| Pricing Model: |

Static Platform Fee + AI Credits. Platform fee covers unlimited non-LLM orchestration across all agents (GRC platform connection management; regulatory database connection; API polling; SMTP dispatch; audit log writes; risk score DW writes). AI Credits consumed only by Goldfinch AI tool invocations and LLM reasoning cycles. |

| Credit Optimization Notes: |

Configure Regulatory Agent Web Crawling to target only the specific publication sections (e.g. new guidance; enforcement actions; consultation papers) rather than full site crawls – reduces Web Crawling credits 40 to 60% while maintaining relevant publication coverage. Batch Financial Risk Agent DW queries for all risk metrics per 4-hour cycle in a single API Tool Call rather than per-metric sequential queries. Cache Knowledge Base risk appetite threshold queries for 7 days (board-approved thresholds change quarterly at most). Configure ESG Risk Agent to run weekly (not daily) for organizations without ESG-linked financing covenants; escalate to daily only during CSRD reporting preparation windows. Route Board Risk Report generation credits to monthly report schedule – avoid re-generating the full Data Analytics dashboard on every daily cycle (update only the KPI delta; generate full dashboard on the report schedule). |

| AI Credits Required: |

Yes – Goldfinch AI agentic systems consume credits across the Enterprise Risk Orchestrator and all 6 Worker Agents per risk monitoring cycle, per document analysis, per regulatory publication processed, and per reflection/retry loop. |

| LLM Steps Count: |

16 to 28 LLM-invoking steps per daily risk intelligence cycle (Orchestrator cross-domain correlation: 3 to 5 LLM steps; each Worker Agent risk assessment: 2 to 4 steps each; Board Risk Report narrative generation: 3 to 5 steps; reflection/retry: 1 to 2 steps per retry) |

| Per-Agent Credit Breakdown: |

Enterprise Risk Orchestrator: 6 to 12 credits per daily cycle (cross-domain correlation + compound risk scoring + Board Report narrative generation + GRC write); Regulatory Agent: 8 to 16 credits per daily monitoring cycle (Web Crawling all configured regulatory bodies + Document Intelligence full-text analysis per new publication + applicability scoring) – highest per-cycle consumer due to regulatory publication volume; Financial Risk Agent: 4 to 8 credits per 4-hour cycle (DW query + VaR/CVaR/LCR Data Analysis computation + threshold comparison), Operational Risk Agent: 2 to 4 credits per monitoring cycle (GRC KRI query + breach severity scoring); Cyber Risk Agent: 3 to 6 credits per daily cycle (cyber risk API query + security posture scoring + regulatory gap analysis); Vendor Risk Agent: 4 to 8 credits per weekly cycle (SRM + D&B API queries + concentration risk scoring + vendor financial health analysis); ESG Risk Agent: 4 to 8 credits per weekly cycle (CSRD/TCFD Web Crawling + ESG score computation + disclosure gap analysis) |

| Goldfinch AI Tool(s) Consuming Credits: |

Vendor Risk Agent – per vendor document analyzed), Data Analysis (Financial Risk Agent, Operational Risk Agent, Cyber Risk Agent, Vendor Risk Agent, ESG Risk Agent, Orchestrator – per risk metric computation cycle), Knowledge Base Vector Search (all 7 agents – per query), Data Analytics with Charts/Graphs/Dashboards (Orchestrator – Board Risk Report and CRO dashboard render), Integration Workflow as Tool (Orchestrator – GRC incident record creation, Board notification, compliance task assignment sub-workflows), Watcher Tools (Orchestrator – continuous risk signal feed monitoring), Web Crawling (Regulatory Agent – per regulatory body publication page crawled; ESG Risk Agent – CSRD/TCFD publications; highest volume credit consumer due to regulatory monitoring breadth), API Tool Call (all 6 Worker Agents – per GRC/DW/cyber risk/vendor risk/ESG data API call), Document Intelligence (Regulatory Agent – per regulatory publication analyzed; |

FAQ

1. What is the Enterprise Compliance and Risk Intelligence system and what does it automate end to end?

The Goldfinch AI risk compliance hub from eZintegrations deploys 7 coordinated AI agents — an Enterprise Risk Orchestrator and 6 domain-specific Worker Agents — to continuously monitor regulatory publications (Regulatory Agent), financial risk metrics against Basel and IFRS 9 thresholds (Financial Risk Agent), operational KRI breaches in the GRC platform (Operational Risk Agent), cyber security posture and DORA compliance (Cyber Risk Agent), third-party vendor risk signals (Vendor Risk Agent), and ESG regulatory obligations (ESG Risk Agent). The Orchestrator cross-correlates all 6 domain signals into a continuous enterprise risk score and generates the Board Risk Report automatically. Deloitte: manual risk monitoring averages a 23-day risk-to-executive-awareness lag; this system compresses it to under 4 hours.

2. How does the multi-agent architecture work?

The Enterprise Risk Orchestrator continuously receives structured risk event messages from all 6 Worker Agents and evaluates them for cross-domain compound risk — a DORA regulatory change combined with a Cyber Risk Agent security posture gap creates a compound regulatory-plus-cyber risk event with higher severity than either signal alone. All 7 agents share a persistent enterprise risk knowledge base containing risk appetite thresholds, regulatory obligation matrices, and historical event precedents, ensuring every agent's domain assessment is grounded in the organization's approved risk framework. Single-domain events below the compound threshold are routed to the relevant domain owner; compound events are escalated to the CRO with full multi-domain context.

3. Which Goldfinch AI tools does this system use?

The system uses 7 of Goldfinch AI's 9 native tools: Watcher Tools (Orchestrator — continuous risk signal feed monitoring), Web Crawling (Regulatory Agent — Basel/EBA/DORA/FDA/ICH/SEC/FCA/OSHA regulatory body sites; ESG Risk Agent — CSRD/TCFD publications), API Tool Call (all 6 Worker Agents — GRC platforms, financial DW, cyber risk APIs, vendor risk APIs, ESG data APIs), Document Intelligence (Regulatory Agent — full regulatory publication analysis; Vendor Risk Agent — vendor financial statement and audit report analysis), Data Analysis (Financial Risk Agent VaR/LCR/CVaR; Operational Risk Agent KRI breach scoring; Cyber Risk Agent security posture; Vendor Risk Agent concentration risk; ESG Risk Agent regulatory disclosure gap; Orchestrator compound risk scoring), Knowledge Base Vector Search (all 7 agents — risk appetite, thresholds, regulatory obligations), and Data Analytics (Orchestrator — Board Risk Report dashboard and CRO brief). Beyond these tools, users can add sanctions screening APIs, geopolitical risk intelligence feeds, and actuarial modeling connectors self-service.

4. How does the system ensure data accuracy and handle errors?

The Orchestrator applies a reflection loop before publishing any compound risk assessment — if cross-domain confidence falls below 0.75, it re-queries the Knowledge Base for relevant risk appetite statements and historical precedents, re-evaluates the cross-domain correlation, and retries up to 3 times before escalating to the CRO with an uncertain flag. The Regulatory Agent applies additional reflection when a regulatory publication has ambiguous applicability scope. Financial Risk Agent metric computations are validated against board-approved calculation methodologies retrieved from the Knowledge Base. All material risk assessments above the hard regulatory limit thresholds (Basel LCR, VaR) trigger immediate human review regardless of agent confidence score.

5. What types of data and documents does this system process?

The system processes: regulatory body publications, guidance documents, enforcement actions, and consultation papers (Regulatory Agent Web Crawling and Document Intelligence); financial risk metrics from DW (market data, credit exposure, liquidity data for Basel III/IV, IFRS 9 computation); GRC platform KRI data from ServiceNow GRC or SAP GRC (Operational Risk Agent); security posture scores and vulnerability data from BitSight or SecurityScorecard (Cyber Risk Agent); supplier financial health reports, D&B risk scores, and vendor audit reports (Vendor Risk Agent Document Intelligence); CSRD, TCFD, and SEC climate disclosure framework publications and MSCI/Refinitiv ESG data (ESG Risk Agent).

6. Who uses this system and in which departments?

Daily operators include the Chief Risk Officer (receives enterprise risk score, compound risk escalations, and CRO brief), Chief Compliance Officer (receives Regulatory Agent compliance obligation alerts and deadline notifications), Chief Information Security Officer (receives Cyber Risk Agent security posture reports and DORA ICT risk alerts), and domain Risk Managers (receive domain-specific risk event notifications). The Board Risk Committee receives the automated Board Risk Report on the configured schedule. The CFO receives Financial Risk Agent hard limit breach notifications immediately. External regulators and auditors access the risk event log and Board Report history via the Goldfinch AI audit dashboard.

7. How does the safety layer and human oversight work?

HITL gates trigger when: a compound risk event exceeds the Critical severity threshold — CRO review required before Board escalation; a new regulatory requirement has a compliance deadline within 90 days — CCO sign-off required on the compliance response plan; a hard financial regulatory limit is breached (Basel LCR below minimum, VaR above board limit) — CFO and CRO immediate notification required regardless of agent confidence; Orchestrator cross-domain confidence falls below 0.75. After 3 retries without resolution, the CRO is escalated with the full agent context and an uncertain flag. All HITL decisions are logged with reviewer identity, decision rationale, and timestamp for Basel, DORA, and FDA regulatory audit documentation.

8. What are the key business benefits and executive KPIs improved?

Key executive KPIs improved include: risk-to-executive-awareness from 23 days (Deloitte benchmark) to under 4 hours, 100% regulatory publication coverage vs. 40 to 60% manual scan coverage, Board Risk Report from 3 to 5 days manual compilation to automated generation on schedule, 30 to 40% GRC operational cost reduction (Gartner), DORA ICT risk monitoring compliance from reactive to continuous, Basel BCBS 239-compliant risk data aggregation for systemically important banks, and the CRO shifts from compiling fragmented domain risk reports to reviewing a continuously updated cross-domain enterprise risk intelligence hub.

Resources

| Blog: |

Amazon Financial Reconciliation: How to Stop Manual Reconciliation-Guide |

|---|---|

| Platform Overview: |

eZintegrations Platform – Enterprise iPaaS, AI Workflows & Agentic AI |

| Demo: |

Book a Demo |

| Goldfinch AI Platform: |

Agentic AI Platform — Goldfinch AI by eZintegrations |

Case Study

| Industry: |

Financial Services / Pan-European Mid-Tier Bank |

|---|---|

| ROI: |

Regulatory examination readiness improvement: estimated €1.2M in avoided regulatory examination remediation cost from proactive vs. reactive compliance management (regulatory penalty avoidance from 100% coverage vs. the prior 55% – based on 2 prior-year examination findings attributable to missed regulatory publications). DORA compliance cost: bank’s DORA preparedness assessment rated “on track” vs. “significantly behind” – estimated €3.5M in DORA non-compliance penalty avoidance (maximum 1% of total annual global turnover for the bank’s size). Compound risk event avoidance: 2 vendor-plus-cyber compound risk events identified 90 minutes after signal vs. average 18 days previously – estimated €1.8M in potential incident cost avoidance from early detection and proactive vendor engagement. Board Risk Report FTE savings: 4.2 days to 3.4 hours per cycle x 12 cycles per year x €520 per FTE-day blended risk team cost = €248,000 annually. Total year-1 conservative |

| Problem: |

A pan-European mid-tier bank with €28B in assets, operations across 9 EU member states, and regulatory obligations across the EBA, ECB, national competent authorities, DORA (from January 2025), Basel III LCR and NSFR requirements, IFRS 9 provisioning, and CSRD climate disclosure obligations operated its risk management function with a team of 48 risk professionals (14 in Regulatory Compliance, 8 in Financial Risk, 6 in Operational Risk, 8 in IT and Cyber Risk, 6 in Third-Party Risk, and 6 in ESG and Sustainability Risk). The risk function operated 6 siloed risk domain tools – each monitored independently by the relevant team, with weekly risk committee meetings as the only cross-domain risk correlation mechanism., The CRO’s risk briefing was compiled manually by a team of 3 Risk Analysts taking 4.2 days on average from each reporting period-end. Key risk gaps identified: DORA compliance monitoring was reactive – the bank had identified its DORA preparedness gap only 8 months before the January 2025 implementation deadline; Regulatory Agent monitoring coverage: the bank’s manual scan covered approximately 55% of relevant EBA and ECB publications (the remaining 45% were identified retrospectively through industry association communications – average 18 days after publication); Compound risk events were invisible to the organization until risk committee – a vendor financial distress event combined with a concurrent cyber risk score deterioration at the same vendor had not been correlated until a 3rd-party incident occurred; Board Risk Report preparation consumed 4.2 FTE-days per cycle across the risk team. |

| Solution: |

Cyber Risk Agent connected to BitSight API for internal security score and all critical vendor security scores (47 critical vendors). Vendor Risk Agent connected to Ariba SRM and Dun and Bradstreet API for financial health monitoring of 340 contracted third parties. ESG Risk Agent configured for CSRD Delegated Acts monitoring, TCFD framework updates, and MSCI ESG data API for supply chain ESG scoring. Knowledge Base Vector Search loaded with: risk appetite framework (board-approved thresholds for all 6 domains), regulatory obligation matrix (24 regulatory bodies x 9 member states), Basel III/IV DORA IFRS 9 compliance methodology documentation, vendor criticality classifications for 340 third parties, and 5 years of Board Risk Report narratives. HITL: compound risk events above Critical require CRO review before Board escalation; financial hard limit breaches trigger CFO and CRO within 15 minutes; DORA ICT incidents require CISO and CRO immediate notification., Deployed the eZintegrations Goldfinch AI risk compliance hub in 24 business days across all 6 risk domains and all 9 EU member state regulatory frameworks. Enterprise Risk Orchestrator configured for cross-domain compound risk scoring against the bank’s own risk appetite framework. Regulatory Agent configured for: EBA, ECB, ESMA, DORA publications, national competent authority (9 member states), FSB, Basel Committee, and IFRS Foundation – 24 total regulatory bodies, automated daily monitoring. Financial Risk Agent connected to Snowflake DW for LCR, NSFR, VaR, and credit concentration metrics (daily computation against Basel III/IV hard limits and board-approved thresholds; IFRS 9 provisioning model monitoring). Operational Risk Agent connected to ServiceNow GRC for all KRI feeds across 12 business lines. |

| Outcome: |

After 6 months: Regulatory publication monitoring coverage from 55% to 100% (all 24 configured regulatory bodies monitored daily, zero publication gaps identified in 6-month audit). Risk-to-CRO-awareness from average 4.2 days (prior manual committee cycle) to average 2.1 hours for material risk events. DORA compliance monitoring: 14 DORA ICT risk requirements identified and compliance response plans initiated – bank rated “on track” by DORA readiness assessment at 3-month pre-implementation review vs. “significantly behind” at the prior-year assessment., Compound risk events identified: 7 in 6 months – including 2 instances of vendor financial distress combined with cyber risk score deterioration at the same critical vendor, both identified by the Orchestrator within 90 minutes of the concurrent signals and routed to the CRO and CISO before the vendor was contacted. Board Risk Report preparation from 4.2 FTE-days to 3.4 hours (full automated generation, CRO review and sign-off). ESG: CSRD Delegated Acts monitoring identified 3 new disclosure requirements with compliance deadlines in the next reporting cycle – all identified within 48 hours of publication vs. prior discovery through industry association (average 22 days after publication). |

Related products

-

How to Automate Enterprise Financial Close Using Multi-Agent AI Orchestration

$150.00

Download

$150.00

Download

-

How to Automate New Product Development Using Multi-Agent AI Stage-Gate Orchestration

$150.00

Download

$150.00

Download

-

Resume Screening Agent

$0.00

Download

$0.00

Download

-

How to Automate Supply Chain Operations Using a Multi-Agent AI Command Center

$150.00

Download

$150.00

Download

{kind=link}